Understanding the Arkansas Foreclosure Timeline

Missing a mortgage payment triggers a chain of events that moves faster than most homeowners expect. Arkansas law allows lenders to pursue foreclosure through two distinct paths, and understanding which one applies to your situation determines how much time you have to act. The state’s foreclosure process can conclude in as few as 60 days under certain circumstances, making quick decisions essential for protecting your credit and financial future.

Non-Judicial vs. Judicial Foreclosure in Arkansas

Arkansas permits both non-judicial and judicial foreclosure, with the method depending on your mortgage documents. If your deed of trust contains a power of sale clause, your lender can foreclose without court involvement. This non-judicial process moves significantly faster, typically completing within 60 to 90 days of the first notice.

Judicial foreclosure requires the lender to file a lawsuit, adding months to the timeline. While this gives you more time, it also increases legal costs that may be added to your debt.

The Statutory Right of Redemption

Arkansas provides a statutory right of redemption only for judicial foreclosures, typically lasting one year, allowing you to reclaim your property by paying the full sale price, plus interest and costs. This right can be waived in most non-judicial foreclosures, which is the most common type in Arkansas. Selling your house before foreclosure in Arkansas offers a more practical path forward than hoping to exercise redemption rights later.

Key Deadlines: Notice of Default to Sale Date

Your lender must provide written notice before accelerating the loan. After the notice period expires, the trustee can schedule a sale with proper public notice. The window between receiving your first warning and losing your home can shrink rapidly, especially with non-judicial foreclosure. Acting within the first 30 days of the missed payment notice gives you the most options.

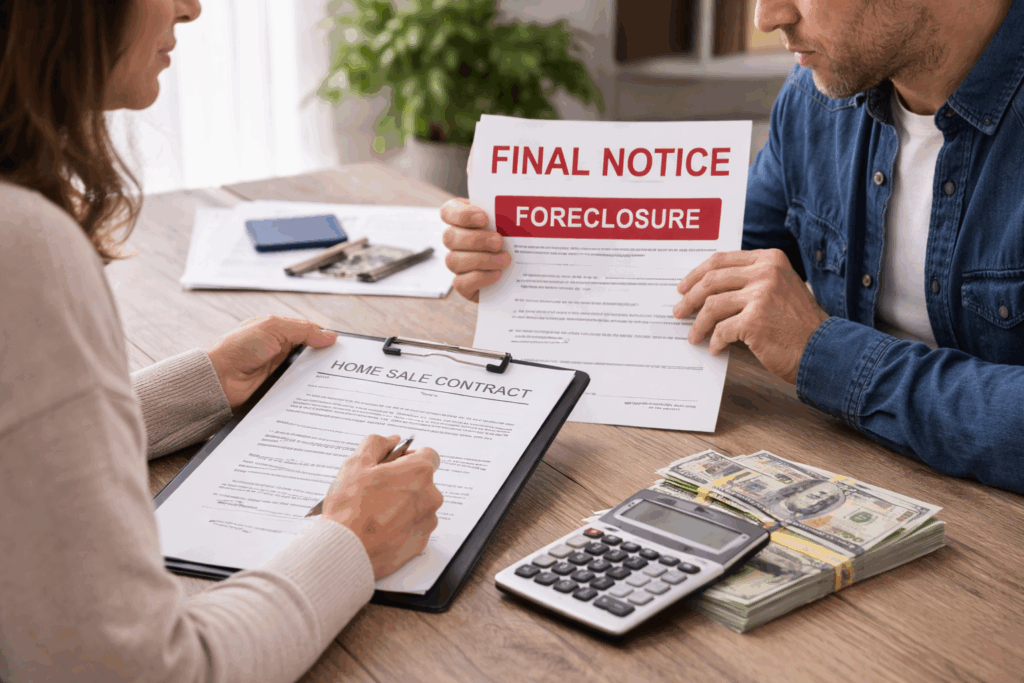

Fast Sale Options to Avoid Credit Damage

A foreclosure stays on your credit report for seven years and can drop your score by 100 to 150 points. Selling before the foreclosure completes can minimize this damage significantly. Multiple fast solutions exist for Arkansas homeowners facing this situation.

Selling to Local Arkansas Cash Home Buyers

Cash buyers like Arkansas Property Buyers specialize in purchasing homes quickly from owners facing distress. These transactions typically close within 7 to 14 days, well within most foreclosure timelines. Cash offers eliminate financing contingencies that cause traditional sales to fall through at the last moment.

The trade-off involves accepting a price below full market value. For homeowners racing against a foreclosure deadline, this discount often makes sense when weighed against the long-term credit damage that can result from foreclosure.

Executing a Short Sale with Lender Approval

When you owe more than your home’s current value, a short sale allows you to sell for less than the mortgage balance with your lender’s approval. The lender agrees to accept the sale proceeds as full satisfaction of the debt, or at least forgives the remaining balance.

Short sales require extensive documentation and lender cooperation. The approval process typically takes 60 to 120 days, so this option works best when you have several months before the scheduled sale date.

The Benefits of an As-Is Sale

Traditional sales often require repairs, staging, and weeks of showings. An as-is sale to an investor eliminates these requirements entirely. You won’t need to fix the leaking roof, update outdated appliances, or even clean out accumulated belongings.

This approach particularly benefits homeowners who lack funds for repairs or whose properties have deferred maintenance issues that would scare off conventional buyers.

Legal and Financial Alternatives to Foreclosure

Selling isn’t always the only option. Several legal mechanisms can help you exit your mortgage obligation while potentially preserving more of your credit standing.

Deed in Lieu of Foreclosure

A deed-in-lieu arrangement involves voluntarily transferring your property title directly to the lender. In exchange, the lender releases you from the mortgage debt without completing the foreclosure process. This option typically damages your credit less than a full foreclosure, though it still appears on your credit report.

Lenders often require proof that you’ve attempted to sell the property before accepting a deed in lieu. They may also require the property to be in reasonable condition and free of junior liens.

Loan Modification and Forbearance Programs

Contact your mortgage servicer immediately upon recognizing payment difficulties. Many lenders offer forbearance programs that temporarily reduce or suspend payments. Loan modifications can permanently adjust your interest rate, extend your term, or reduce principal.

These programs work best when financial hardship is temporary. If your income has permanently decreased or you simply want to exit the property, selling remains the cleaner solution.

Steps to Sell Your Arkansas Home Quickly

Speed matters when foreclosure looms. A systematic approach helps you maximize value while meeting critical deadlines.

Determining Current Market Value and Equity

Pull comparable sales data from your neighborhood to estimate your home’s current market value. Subtract your remaining mortgage balance, any second mortgages, and outstanding liens to calculate your equity position. This number determines which sales options are financially sound.

If you have positive equity, you have more flexibility. Negative equity situations may require short sale negotiations or other creative solutions.

Communicating with Your Mortgage Servicer

Call your servicer’s loss mitigation department rather than standard customer service. Explain your situation honestly and ask about all available options. Request written confirmation of any agreements and document every conversation with dates, names, and reference numbers.

Some servicers will delay foreclosure proceedings while you actively market the property. Getting this commitment in writing protects you from unexpected acceleration.

Gathering Essential Documentation for an Urgent Sale

Prepare these documents before listing or contacting buyers: your current mortgage statement, property deed, recent tax assessments, HOA documents if applicable, and any existing inspection reports. Having paperwork ready accelerates closing timelines significantly.

For short sales, you’ll also need hardship letters, bank statements, tax returns, and pay stubs to submit with your lender’s required package.

Protecting Your Future After a Pre-Foreclosure Sale

Completing a sale before foreclosure protects more than your credit score. It preserves your ability to purchase another home sooner, maintains your employment prospects in industries that check credit, and eliminates the stress of legal proceedings.

Working with experienced local buyers who understand Arkansas foreclosure timelines can make the difference between a successful sale and losing your home at auction. Arkansas Property Buyers provides fair cash offers within 24 hours, handling properties in any condition without requiring repairs, commissions, or fees.

Frequently Asked Questions

How long do I have to sell my house before foreclosure in Arkansas?

The timeline varies based on foreclosure type. Non-judicial foreclosure can be completed in as little as 60 to 90 days, while judicial foreclosure takes several months longer. Your best window for action is within 30 days of receiving a default notice.

Will selling before foreclosure hurt my credit?

Selling before foreclosure typically causes less credit damage than a completed foreclosure. A regular sale has minimal impact, while a short sale may reduce your score by 50 to 80 points compared to 100 to 150 points for foreclosure.

Can I sell my house if I owe more than it’s worth?

Yes, through a short sale with lender approval. The lender agrees to accept less than the full mortgage balance. This process requires documentation of financial hardship and typically takes 60 to 120 days for approval.

Do I need to make repairs before selling to avoid foreclosure?

No. Cash buyers and investors purchase properties as-is, eliminating repair requirements. This saves time and money when you’re facing tight foreclosure deadlines.

What happens to my equity if I sell before foreclosure?

Any equity remaining after paying off your mortgage, closing costs, and fees belongs to you. Selling before foreclosure preserves this equity rather than losing it at auction.

Moving Forward with Confidence

Facing foreclosure feels overwhelming, but Arkansas homeowners have real options for protecting their financial future. Acting quickly, understanding your timeline, and choosing the right sale method can mean the difference between a fresh start and years of credit recovery. If you need a fast solution, consider reaching out to Arkansas Property Buyers for a no-obligation cash offer that can close on your timeline.